TBA V CTS the facts

- Bob Brogan

-

Topic Author

Topic Author

- Administrator

-

- Posts: 82524

- Thanks: 6461

TBA V CTS the facts

10 years 9 months ago

Breeding Industry Sales Facts

Our industry was rocked last week by CTS’s announcement of two sales in Johannesburg coinciding with and/or in very close proximity to the TBA/BSA’s announced dates of the long established RTR Sale and NYS.

In a small market like ours it is particularly true, and has been long accepted, that the sales have to be spread out to allow buyers to “re-group”. Thus vendors get better prices and sales companies get better income. In 2011, BSA held the Premier Sale at the CTICC followed by the Summer Sale in March immediately preceding the two-day Vintage Sale and the vendors took a hammering in March. It just does not make good business sense to hold sales on top of each other.

As soon as I heard rumours of this move, I phoned Chris van Niekerk who did not take my call and nor has he returned it. There is much speculation that CTS have launched a hostile assault on BSA, which could pose a threat to the future of the sales activities of our Association.

I hope that breeders will give extra careful consideration of the facts as they make their sales entries over the next few months.

· Buyers

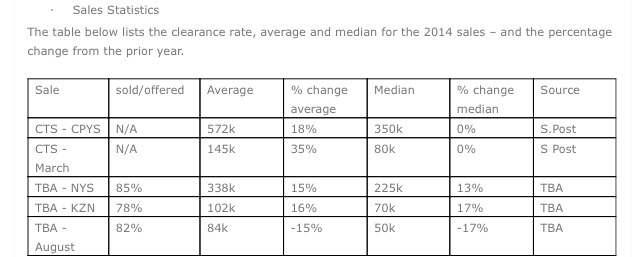

As a vendor, it is important to consider whether the sale is supported by a wide spread of buyers as this should translate into better demand at all levels. At NYS in 2014, the top 25 buyers were responsible for only 65% of the aggregate of the sale. At KZN and August sales, the top 25 buyers spent 61% of the total. This indicates an excellent spread of buyers, so a vendor can be reasonably expectant that not only will there be a buyer but also the very necessary underbidder so that a fair price is realised. This is far more attractive proposition than a sale with one dominant buyer.

It can be seen that the strong buyer spread and support resulted in good figures for TBA sales. The clearance rates ranged from 78% to 85%, with the average and (the more revealing) median both posting double-digit increases at NYS and KZN. It is worth pointing out that although the figures for August 2014 sale were down by average and median, the results were on the back of very strong sale in 2013 which had gains of over 40% in both statistics.

· Sales entities

The TBA runs sales on a truly independent basis where “all men count … but none too much”. The sales activity enables the Association to earn profits that it can then apply for the benefit of breeders and the Thoroughbred breed, these include equine health, vaccination programmes, research, quarantine and trade. For many years the TBA funded its industry obligations entirely from profits, but the loss of significant market share necessitated the imposition of the foal levy. Although the foal levy covers the majority of the obligation to equine research, there is a shortfall that is paid by the TBA. The TBA’s financial results are made public and the TBA’s contributions to industry are detailed in black-and-white.

CTS claim that it benefits industry by “improving the bloodstock platform” by way of guaranteed payouts and bringing international people to its sales.

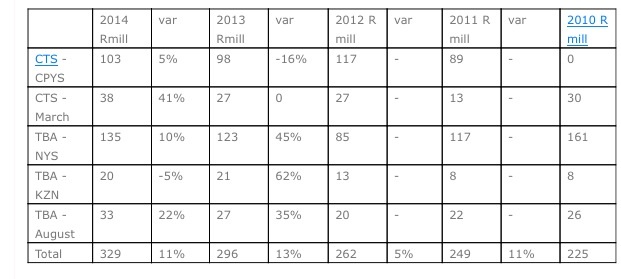

Finally, I would like to end with some thoughts on competition. Competition is generally held to be a good thing because, so the logic goes, the consumer (vendor) will get a better product (higher proceeds) at a lower cost (levy etc) from the competing suppliers. Perhaps the entry of CTS in 2012 has been a benefit to the overall sales market? The table below details the turnover (R million) at the five sales over the last five years.

NB 2011 CPYS run by TBA.

NB 2011 and 2010 March figure = Cape + Equimark

The combined aggregates at CPYS and March from 2012 to 2014 have slightly declined from R144 million to R141 million. In comparison, over the same period, TBA’s total NYS/KZN/August aggregate has grown by 59% from R118 million to R188 million. So the total market for unbroken yearlings and two year olds has increased by over 25% between 2012 and 2014, but the growth has actually come from TBA sales.

Perhaps the competition has resulted in lower costs to the consumer? In 2011, aside from the new CPYS run by TBA, commissions were 7% for a national sale and 4% for regional. In 2012, CTS set their commission at 8%, and the TBA, having to maintain its industry funding obligations despite the massive loss of income, had no choice but to increase all commissions to 8% and re-introduce a foal levy.

Lets quantify the cost of this on the breeders’ pockets:

1% extra commission on the total yearling market of R329million = R3.29 million

3,000 foals at R500 per foal = R1.50 million

Total = R4.79 million

This competition has actually resulted in the 300 or so breeders paying an extra R4.79 million per annum.

The essence of competition is that it is all about choice for the customer. When faced with a choice, it is essential to be well-informed so as to make a wise selection. The facts as laid out above are all important considerations for each and every breeder in making their choices as regards sales entries for 2015.

Yours sincerely

Susan Rowett

Chairman

Our industry was rocked last week by CTS’s announcement of two sales in Johannesburg coinciding with and/or in very close proximity to the TBA/BSA’s announced dates of the long established RTR Sale and NYS.

In a small market like ours it is particularly true, and has been long accepted, that the sales have to be spread out to allow buyers to “re-group”. Thus vendors get better prices and sales companies get better income. In 2011, BSA held the Premier Sale at the CTICC followed by the Summer Sale in March immediately preceding the two-day Vintage Sale and the vendors took a hammering in March. It just does not make good business sense to hold sales on top of each other.

As soon as I heard rumours of this move, I phoned Chris van Niekerk who did not take my call and nor has he returned it. There is much speculation that CTS have launched a hostile assault on BSA, which could pose a threat to the future of the sales activities of our Association.

I hope that breeders will give extra careful consideration of the facts as they make their sales entries over the next few months.

· Buyers

As a vendor, it is important to consider whether the sale is supported by a wide spread of buyers as this should translate into better demand at all levels. At NYS in 2014, the top 25 buyers were responsible for only 65% of the aggregate of the sale. At KZN and August sales, the top 25 buyers spent 61% of the total. This indicates an excellent spread of buyers, so a vendor can be reasonably expectant that not only will there be a buyer but also the very necessary underbidder so that a fair price is realised. This is far more attractive proposition than a sale with one dominant buyer.

It can be seen that the strong buyer spread and support resulted in good figures for TBA sales. The clearance rates ranged from 78% to 85%, with the average and (the more revealing) median both posting double-digit increases at NYS and KZN. It is worth pointing out that although the figures for August 2014 sale were down by average and median, the results were on the back of very strong sale in 2013 which had gains of over 40% in both statistics.

· Sales entities

The TBA runs sales on a truly independent basis where “all men count … but none too much”. The sales activity enables the Association to earn profits that it can then apply for the benefit of breeders and the Thoroughbred breed, these include equine health, vaccination programmes, research, quarantine and trade. For many years the TBA funded its industry obligations entirely from profits, but the loss of significant market share necessitated the imposition of the foal levy. Although the foal levy covers the majority of the obligation to equine research, there is a shortfall that is paid by the TBA. The TBA’s financial results are made public and the TBA’s contributions to industry are detailed in black-and-white.

CTS claim that it benefits industry by “improving the bloodstock platform” by way of guaranteed payouts and bringing international people to its sales.

Finally, I would like to end with some thoughts on competition. Competition is generally held to be a good thing because, so the logic goes, the consumer (vendor) will get a better product (higher proceeds) at a lower cost (levy etc) from the competing suppliers. Perhaps the entry of CTS in 2012 has been a benefit to the overall sales market? The table below details the turnover (R million) at the five sales over the last five years.

NB 2011 CPYS run by TBA.

NB 2011 and 2010 March figure = Cape + Equimark

The combined aggregates at CPYS and March from 2012 to 2014 have slightly declined from R144 million to R141 million. In comparison, over the same period, TBA’s total NYS/KZN/August aggregate has grown by 59% from R118 million to R188 million. So the total market for unbroken yearlings and two year olds has increased by over 25% between 2012 and 2014, but the growth has actually come from TBA sales.

Perhaps the competition has resulted in lower costs to the consumer? In 2011, aside from the new CPYS run by TBA, commissions were 7% for a national sale and 4% for regional. In 2012, CTS set their commission at 8%, and the TBA, having to maintain its industry funding obligations despite the massive loss of income, had no choice but to increase all commissions to 8% and re-introduce a foal levy.

Lets quantify the cost of this on the breeders’ pockets:

1% extra commission on the total yearling market of R329million = R3.29 million

3,000 foals at R500 per foal = R1.50 million

Total = R4.79 million

This competition has actually resulted in the 300 or so breeders paying an extra R4.79 million per annum.

The essence of competition is that it is all about choice for the customer. When faced with a choice, it is essential to be well-informed so as to make a wise selection. The facts as laid out above are all important considerations for each and every breeder in making their choices as regards sales entries for 2015.

Yours sincerely

Susan Rowett

Chairman

Please Log in or Create an account to join the conversation.

- Bob Brogan

-

Topic Author

- Administrator

-

- Posts: 82524

- Thanks: 6461

Re: TBA V CTS the facts

10 years 9 months ago

I thought this was a very good article, and should make you guys think

Please Log in or Create an account to join the conversation.

- @teamwildracing

-

- New Member

-

- Thanks: 0

Re: TBA V CTS the facts

10 years 9 months ago

Gloves are off and the battle lines firmly drawn. Will be very interesting to see how the breeders respond. For me, a very small breeder, I've decided to stay with TBA but will be watching closely. Susan makes a very strong case and I love her gusto but ultimately I think for many the proof will be in the pudding. There is no doubt she is going to need strong public support from big brand breeders.

Please Log in or Create an account to join the conversation.

- Over the Air

-

- Platinum Member

-

- Posts: 2948

- Thanks: 721

Re: TBA V CTS the facts

10 years 9 months ago

A family friend bred for years albeit on a small scale. I recall vividly being amazed at a story he told me about how he had been screwed by a well known trainer who had later been warned off. This trainer bought one of his horses and could not pay. 8 months after the sale my friend arrived unannounced at the trainers yard and repossessed his own horse. He told me that the TBA did little to nothing to assist in getting the outstanding cash and whenever he started getting vocal, he was referred to the rules. These apparently stated that the risk was entirely the breeders and the TBA were not liable in any way for defaulters or something to that effect. Competition is good. The TBA must evolve or crumble. Should I be a breeder I would most definitely support CTS if the only other choice was the TBA

Please Log in or Create an account to join the conversation.

- Garth

-

- Junior Member

-

- Posts: 45

- Thanks: 0

Re: TBA V CTS the facts

10 years 9 months ago

I would support the TBA.

CTS is controlled by Jooste/ Van Niekerk - who are trying to take over every aspect of racing - not good news for the small owner.

CTS is controlled by Jooste/ Van Niekerk - who are trying to take over every aspect of racing - not good news for the small owner.

Please Log in or Create an account to join the conversation.

- Bob Brogan

-

Topic Author

- Administrator

-

- Posts: 82524

- Thanks: 6461

Re: TBA V CTS the facts

10 years 9 months ago@teamwildracing wrote: Gloves are off and the battle lines firmly drawn. Will be very interesting to see how the breeders respond. For me, a very small breeder, I've decided to stay with TBA but will be watching closely. Susan makes a very strong case and I love her gusto but ultimately I think for many the proof will be in the pudding. There is no doubt she is going to need strong public support from big brand breeders.

Summerhill have sent a press release, but not to abc so I won't post it

")

Please Log in or Create an account to join the conversation.

- @teamwildracing

-

- New Member

-

- Thanks: 0

Re: TBA V CTS the facts

10 years 9 months ago

www.sportingpost.co.za/2014/09/ready-to-...summerhill-responds/

Makes interesting points and on face value looks like a considered decision. Like I said one to watch, yes competition is good and many on here know I mean that but for it to lift the industry it must be fought across fair lines.

Makes interesting points and on face value looks like a considered decision. Like I said one to watch, yes competition is good and many on here know I mean that but for it to lift the industry it must be fought across fair lines.

Please Log in or Create an account to join the conversation.

Time to create page: 0.108 seconds